|

The WTI crude oil spot price jumped over 3.5% for the week to close on Friday at $47.84 per barrel, while the Brent crude spot price gained 2.81% to close at $50.84 per barrel, after the EIA weekly report for U.S. oil inventory showed that domestic crude supplies declined by 5.25 million barrels to 522.53 million barrels, excluding the Strategic Petroleum Reserve, in the week ending May 5, compared to the S&P Global Platts forecast for a stockpile decline of 1.8 million barrels. The American Petroleum Institute, or API, inventory data on Tuesday showed a U.S. crude inventory draw of 5.8 million barrels. The net imports for crude oil in the week ending May 5, was 6.93 million barrels per day, or bpd, down 799,000 bpd compared to the previous week, as crude imports dropped 644,000 bpd while exports surged 155,000 bpd.

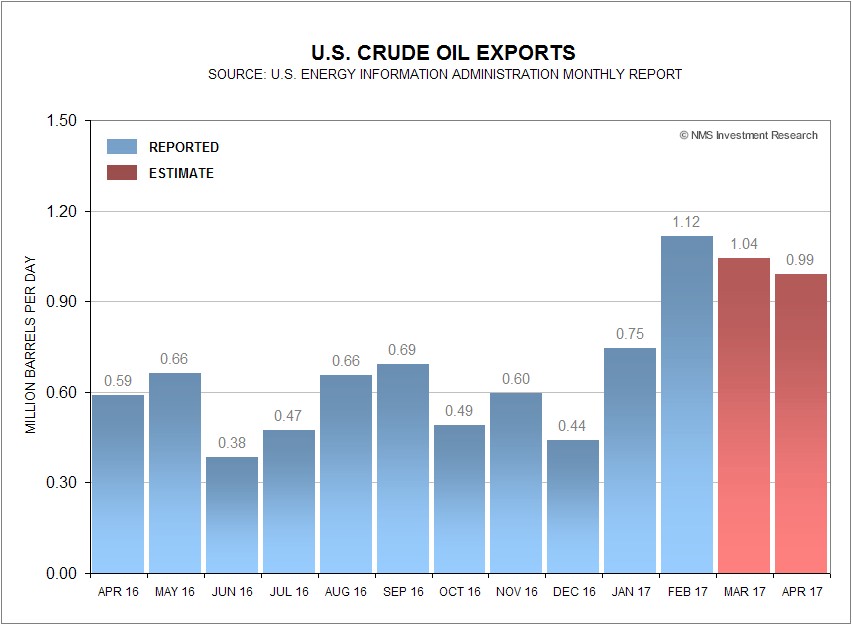

The EIA monthly reports for U.S. crude oil imports and exports, released at the end of April, showed that the U.S. crude oil imports in February declined 0.3% year-on-year to 7.89 million bpd, while exports skyrocketed 198.3% to 1.12 million bpd. Based upon our estimation, U.S. crude oil exports could stay near 1 million bpd in March and April, making the OPEC production cuts to ease the glut near term less likely. The EIA monthly reports for March 2017 is due on May 31.

Separately, the EIA said the weekly U.S. crude oil production increased another 21,000 bpd, for the week ending May 5, to 9.31 million bpd. U.S. crude oil output increased 53,000 bpd to an average of 9.31 million bpd in May, compared to an April average of 9.26 million bpd. Output has fallen just 2.98% from the peak level of 9.60 million bpd in June 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose another 9 to 712, compared to 316, when the rig count hit the low on June 6, 2016.

S&P 500 Summary: +6.79% YTD as of 05/12/17

Barclay Hedge Fund Index: +3.57% YTD

Outperforming Sectors: Information technology +17.78 YTD, Consumer discretionary +10.39% YTD, and Healthcare +9.07% YTD.

Underperforming Sectors: Consumer staples +6.07% YTD, Utilities +6.02% YTD, Materials +5.66% YTD, Industrials +5.48% YTD, Real Estate +1.68% YTD, Financials +1.01% YTD, Energy –10.31% YTD, and Telecommunication services –10.85%

YTD. |