|

The Thailand SET opened with a 0.6% gap up and moved higher to close at 1,549.53 on Tuesday in response to the weak U.S. payrolls report, which said on Friday that employers added just 126,000 workers in March with the unemployment rate holding steady at 5.5%. It was a huge miss as economists expected non-farm payrolls to rise 245,000. The trading was sluggish as the Thailand SET traded sideways after the Tuesday surge, to close at 1,547.83 on Friday, up 0.77% for the week.

The big story was the Fed minutes, which was released on Wednesday, showing divergence among the Fed members on the appropriate timing of the first rate hike. Several Fed members said the central bank is likely to raise its benchmark interest rate in June, but "others" said the move will probably occur "later in the year".

The currency and bond markets are signaling that the first rate hike might be coming as early as June. The U.S. Dollar index (DXY), a weighted geometric index of the value of the U.S. dollar relative to a basket of six major currencies, rose 1.72% for the fifth straight day to close at 99.35 on Friday, while the 10-year U.S. Treasury yield jumped 1.7% to close at 1.9526%.

The EUR/USD tumbled 3.48% to close at U.S. $1.0596 dollars per euro for the week, as the currency markets raised concern that Greece would not be able to pay the 450 million euro loan installment to the International Monetary Fund (IMF) due on Thursday. According to the IMF’s chief Christine Lagarde, Greece's government made the loan installment payment, narrowly avoiding default.

The EUR/USD is also under the pressure as Ms. Lagarde said that the prospects for economic growth in the euro region remain gloomy and unemployment is stuck at high levels, while the United States will remain the largest economic power in the world.

The DXY received further support from a weak Japanese yen as the Reserve Bank of Australia (RBA) decided on Tuesday to hold the benchmark interest rates at 2.25%. The AUD/JPY surged 1.19% to close at 91.81 yen per Australian dollar, while the USD/JPY surged 1.18% to close at 120.33 yen per dollar on the day that the RBA made its announcement.

The USD/THD exchange rate inched up 0.44% to close at 32.549 baht per dollar, while the 10-year Thailand Government bond yield stayed at 2.74%, up 0.01% for the week. The THB/JPY gained 0.52% to close at 3.69 yen per baht, while the EUR/THB tumbled 2.96% to close at 34.527 baht per euro on Friday.

The capital outflows and foreign investor selling might pick up a bit as the yield spread between the U.S. 10-Year Treasury and the Thailand 10-Year Government bond has narrowed to 0.7874%. The rising Thai baht, against the euro and the Japanese yen, could put more pressure on exporters.

Separately, the IMF slightly revised its forecast for Thailand's 2015 economic growth up on Friday, to 3.7% from 3.5%, citing some rebound in consumption and in private investment. The IMF's revised forecast is very much in line with the latest economic growth estimate of 3.8% by the Bank of Thailand (BOT).

Two weeks ago, Kasikorn Research Centre trimmed its Thailand GDP forecast for 2015 from 4.0% to just 2.8%, while the Asian Development Bank (ADB), a Metro Manila, Philippines-based Asia-Pacific region multilateral finance institution, said the Thailand GDP for this year is now 3.6% as weak exports, low farm prices and high household debts persist.

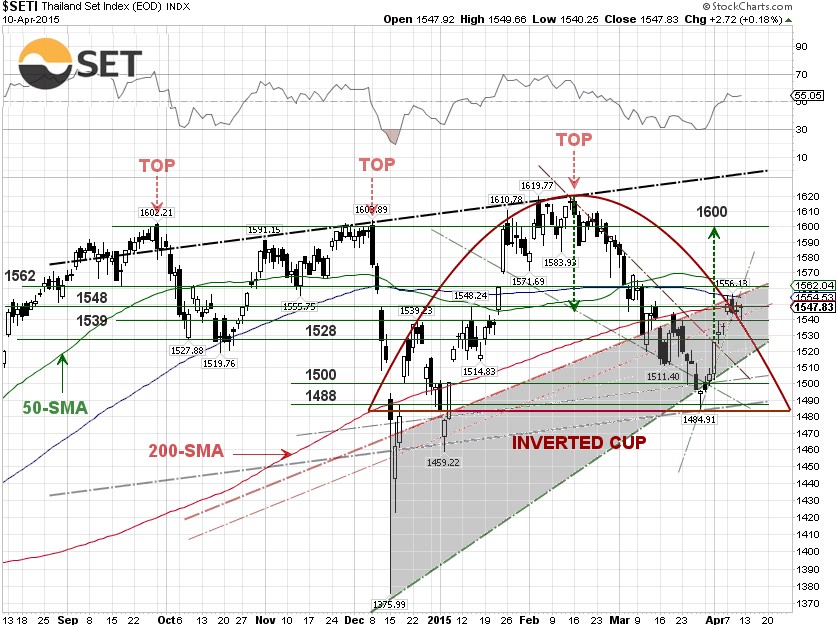

From our technical viewpoint, the Thailand SET is running into trouble again at the 1,548 and 1,539 levels, as the index was unable to break the key moving averages to the up side. A successful breakout of the key moving averages could send the Thailand SET towards 1,600, the projected price for a falling wedge breakout event.

The inverted cup and bearish rising wedge patterns have now emerged in the chart pattern. One may want to pay attention that the Thailand SET doesn’t fall back into the inverted cup pattern, as it could be interpreted as a sell signal for momentum traders. If the market decides to pull back, there is a key technical support at 1,528. |