|

The WTI crude spot price gained 1.69% for the week, closing at $49.31 per barrel on Friday, while the Brent crude spot price was up 0.94% for the week to close at $51.76 per barrel, after a bullish EIA weekly report. Crude prices responded mutedly to the Reuters report Friday saying that non-OPEC producers delivered 64% of pledged oil output cuts in February. The report also said Russia will cut output by the full amount it had pledged, which is 300,000 barrels per day, or bpd, by the end of April. A weak U.S. dollar might contribute to a jump in crude prices, but the correlation between crude oil prices and the dollar is poor.

The contract for difference, or CFD, rollover, is on Sunday, when traders swap a matured contract price with a new one before the old contract expires, so the crude prices will be volatile next week. Traders were skeptical and already bearish on crude oil, as speculative short positions in WTI crude oil futures contracts held by money managers jumped to 128, 947 contracts as of March 14, 2017, an increase of 110% or 67,779 contracts from previous week, according to data from the U.S. Commodity Futures Trading Commission, or CFTC.

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies decreased by 0.237 million barrels to a near all-time high of 528.16 million barrels, excluding the Strategic Petroleum Reserve, in the week ending March 10, compared to the S&P Global Platts forecast for a stockpile increase of 3.5 million barrels. The American Petroleum Institute, or API, inventory data on Tuesday showed a U.S. crude inventory decrease of 0.531 million barrels.

Separately, the EIA said the weekly U.S. crude oil production increased 21,000 bpd for the week ending March 10, to 9.109 million bpd. U.S. crude oil output increased 61,000 bpd to an average of 9.058 million bpd in March, compared to a February average of 8.997 million bpd. Output has fallen about 5.65% from the peak level of 9.60 million bpd in June 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose another 14 to 631, compared to 316, when the rig count hit the low on June 6, 2016.

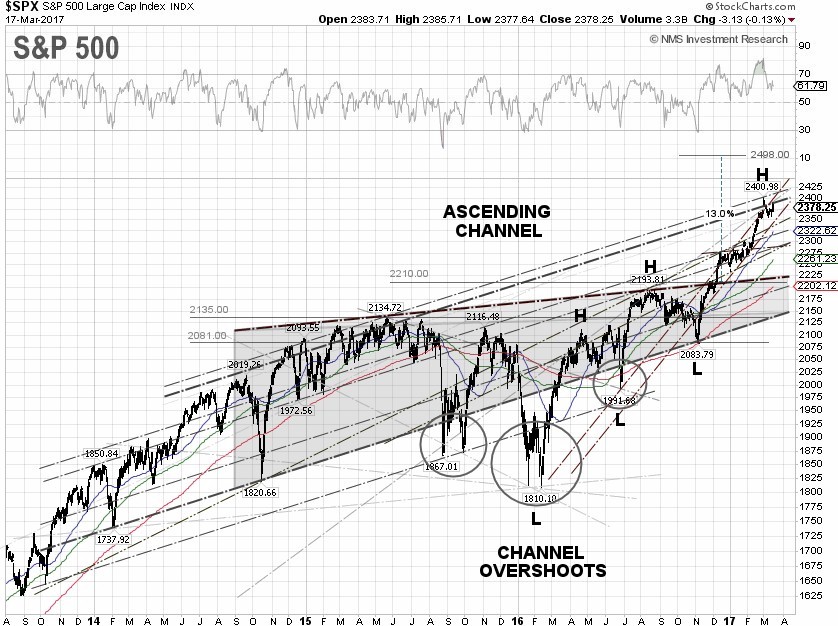

S&P 500 Summary: +6.23% YTD as of 03/17/17

Barclay Hedge Fund Index: +2.47% YTD

Outperforming Sectors: Information technology +11.94 YTD, Healthcare +9.16% YTD, Consumer discretionary +7.41% YTD, Consumer staples +6.53% YTD, and Financials +5.26% YTD.

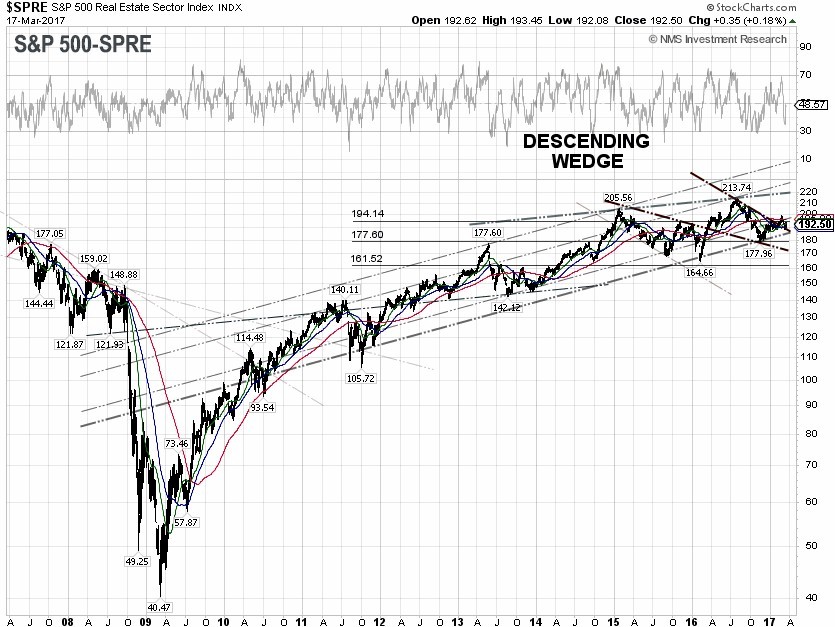

Underperforming Sectors: Materials +5.52% YTD, Utilities +5.43% YTD, Industrials +4.94% YTD, Real Estate +1.19% YTD, Telecommunication services –2.44% YTD, and Energy –7.70%

YTD. |