|

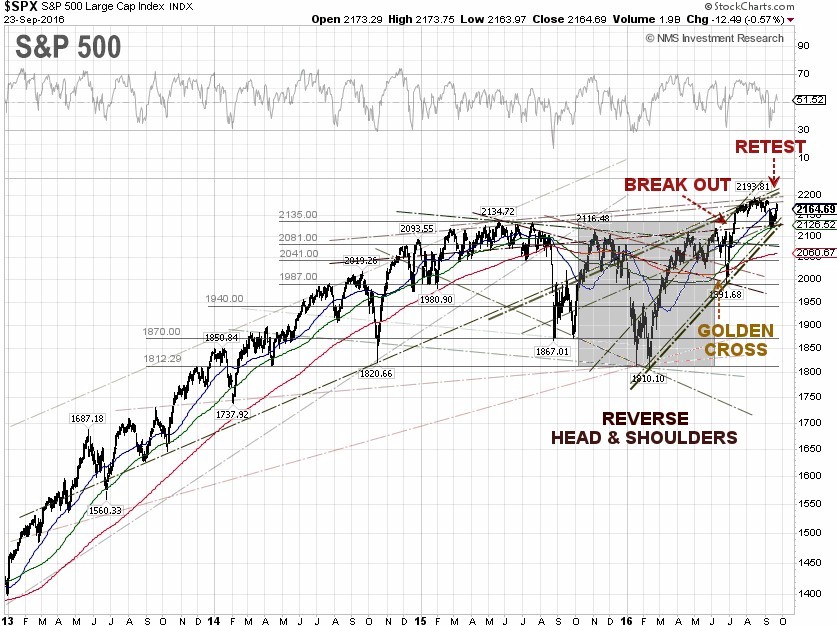

The S&P 500 managed to gain 1.19% for the week, to close on Friday at 2,164.69, despite several “unusual” trading activities on Friday, including a Reuters report from anonymous sources of no OPEC output deal between Saudi Arabia and Iran, which sent crude prices down almost 4% and slammed the S&P 500 Energy sector by 1.26%.

Shares of Apple Inc. (NASDAQ:AAPL) tumbled 2.68% at 13:30 EST Friday, after CNBC reported that Germany’s largest market research company Nuremberg-based GfK

(Gesellschaft für Konsumforschung) sent out a report that supposedly raised concerns about sales of the latest

iPhone. GfK confirmed the existence of the report to CNBC, but said it was exclusively for subscribers and would not divulge the contents.

It wasn’t much of a surprise on Wednesday when the U.S. Federal Reserve decided to keep its benchmark interest rate unchanged and pretty much told everybody, “See you in December for a rate decision, maybe”.

The U.S. economy is showing signs of a significant slowdown. The Federal Reserve Bank of New York knocked 50 basis points off its third-quarter and fourth-quarter 2016 GDP forecast on Friday, to 2.3% and 1.2%, respectively, from the previous 2.8% and 1.7%, citing U.S. data in the past two weeks, from manufacturing, retail sales, housing and construction, that has been negative. Taking the latest New York Fed forecast into account, the pace of U.S. GDP annual growth will be just 1.4% year-on-year, the slowest growth since 2009. The current blue chip consensus U.S. GDP 2016 forecast is 1.8%.

On Tuesday, the Federal Reserve Bank of Atlanta revised its third-quarter 2016 GDP forecast 10 basis points downward, to 2.9% from the previous 3.0%, after the U.S. Department of Commerce said that housing starts fell 5.8% last month from July, to an annual rate of 1.142 million. In fact, housing starts have been volatile, with a deviation of as much as 20% on month-on-month basis.

London-based IHS Markit said on Friday that its flash U.S. manufacturing purchasing managers index fell to 51.4 in September from 52, marking the lowest level since June, citing weak new orders, especially from exports clients. Any reading above 50 indicates improving conditions. U.S. manufacturing PMI has been on downhill slide since the index reached an all time high of 57.90 in August of 2014.

Prior to the Fed rate decision on Wednesday, the Bank of Japan (BOJ) announced a monetary policy reboot to get Japan out of its risk-aversion mode, by shifting from targeting the volume of asset purchases to the yield curve, as a flat yield curve hurts sentiment. According to Bloomberg, the short-term target will be the negative 0.1% interest on excess reserves

(IOER) rate that the BOJ placed on a portion of the cash reserves that commercial banks park at the central bank. The long-term target rate was set at around zero percent for the 10-year Japanese government bonds

(JGBs). The BOJ also pledged to keep easing until inflation overshoots its 2% inflation target.

For the week, the U.S. dollar index declined 0.69%, to close at 95.392 on Friday. The yield of 10-year U.S. Treasury Notes tumbled 4.71% for the week to close at 1.62%, while the yield spread between the 10-year and 2-year U.S. Treasury Notes stands at 0.85 percentage points, a level not seen since late 2007. The global bond markets are rattled, as the 10-year JGB yield tumbled over 40% to negative 0.048% at the close on Friday, while the 10-year German bund yield printed at negative 0.081%.

The WTI crude price, which surged earlier in the week following bullish weekly inventory reports and a weak U.S. dollar, took a U-turn on Friday and tumbled 3.97%, while the Brent crude spot price tanked 2.93% after Reuters reported that Saudi Arabia was ready to cut output to levels seen early this year in exchange for Iran freezing production at the current level, which is 3.6 million barrels per day (bpd).

According to Reuters, the information came from a source familiar with the matter, while three more sources confirmed that the Saudi offer was presented to the Iranian government. The market thinks that Iran will not agree to such a proposal at the informal OPEC meeting next week, or any time soon. The WTI crude spot price still managed to close up 1.97% for the week, at $44.48 per barrel on Friday, while the Brent crude spot price was practically unchanged for the week to close at $46.00 per barrel.

The EIA weekly U.S. oil inventory report on Wednesday showed a decrease of 6.2 million barrels to 504.6 million barrels, excluding the Strategic Petroleum Reserve, in the week ending September 16, compared to S&P Global Platts analysts’ expectations for a rise of 2.8 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory decrease of 7.5 million barrels.

Separately, the EIA said the weekly U.S. crude oil production increased by 19,000 bpd for the week ending September 16, 2016, to 8.512 million bpd. Weekly U.S. crude oil output has fallen about 11.43% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose by 2 to 418, compared to 316, when the rig count hit the low on June 6, 2016.

The best performing S&P 500 sectors for the week were Utilities, Telecommunication services, and Industrials up 3.37%, 1.92% and 1.83%, respectively. The worst performing sectors for the week were Financials and Energy, down 0.83% and 0.1%, respectively.

S&P 500 Summary: +5.91% YTD as of 09/23/16

Barclay Hedge Fund Index: +3.43% YTD

Outperforming Sectors: Utilities +17.61% YTD, Telecommunication services +15.40% YTD, Energy +10.89% YTD, Information technology +10.24% YTD, Materials +8.66% YTD, and Industrials +7.82% YTD.

Underperforming Sectors: Consumer staples +5.69% YTD, Consumer discretionary +1.94% YTD, Healthcare +1.53% YTD, Financials +0.01% YTD, and Real Estate +0.00%.

Disclosure: Long position in AAPL and no recommendation. |