|

The U.S. Bureau of Labor Statistics

(BLS) said on Friday that U.S. total nonfarm payrolls increased by a seasonally adjusted 151,000 jobs last month, missing Wall Street economists' forecast of an 180,000 gain. Both the U-3 and U-6 unemployment rates remained at 4.9% and 9.7%, respectively. The change in total nonfarm payrolls employment for June was revised down from +292,000 to +271,000, and the change for July was revised up from +255,000 to +275,000. The total nonfarm payrolls growth reflects the weak U.S. GDP for the first-half 2016, which was below 1%, due in part to the Fed rate hike in December 2015.

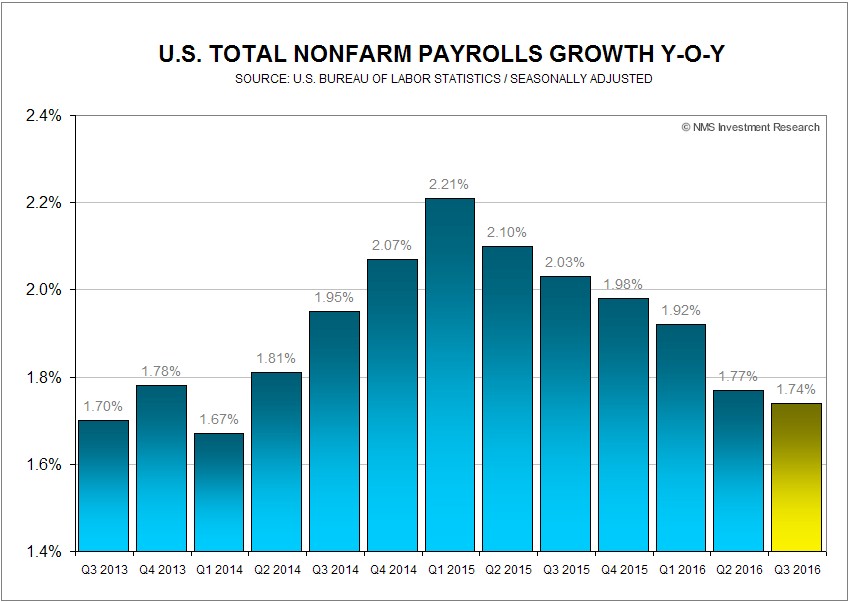

The BLS also said that the total seasonally adjusted nonfarm payrolls, as of August 2016, stands at 144,598 million. If 213,000 jobs, the average of July and August, are added for September, total nonfarm payrolls growth will be 1.74% year-on-year for the third-quarter 2016, the slowest since the second-quarter 2014. One can argue that slow growth in total nonfarm payrolls could be due to lack of qualified workers as the labor market approaches maximum employment, which is vaguely defined by the Fed.

The labor force participation rate remained at 62.8%, since some 94.4 million Americans were not in the labor force in August. From the household survey, the number of persons who are not in the labor force but want a job now registered at 5.83 million, meaning the unemployment rate would be 8.6% if this group of persons was considered as unemployed.

There was more bad news for the U.S. economy during the week, as the Institute of Supply Management (ISM) manufacturing index surprisingly came in on Thursday at 49.4, missing the estimate of 52, and down from 52.6 in July. The index reading below 50 indicates contraction. The ISM said new orders, order backlogs, and employment, all shrank.

The U.S. Dollar index inched up 0.32% for the week, to close on Friday at 95.844, as some Fed officials continue to insist on September rate hike, while the yield of the 10-year U.S. Treasury Note declined 1.23% to close at 1.60% on Friday. The yield spread between the 10-year and 2-year U.S. Treasury Notes widened to 0.8 percentage points at the close on Friday, a level not seen since November 2007.

The probability of a 25 basis point rate hike at the next FOMC meeting on September 21 dropped 3 percentage points, to 21.0%, after the release of the employment situation report on Friday, while the probability of a no change in monetary policy rose to 79.0%, based on the CME Group 30-day Fed Fund futures prices as of September 2. |