|

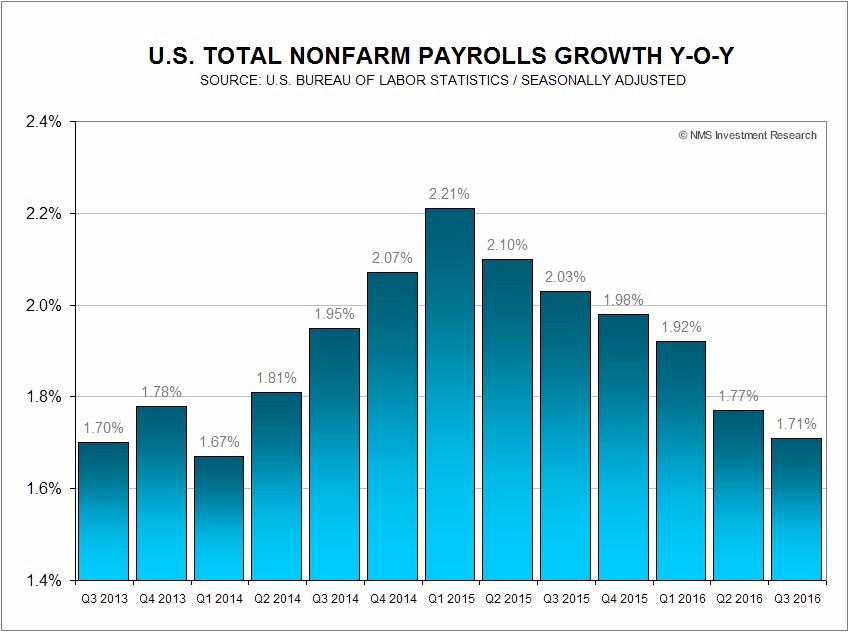

Weak economic data prompted the Federal Reserve Bank of Atlanta to revise its third-quarter 2016 GDP forecast another 10 basis points downward on Friday, to 2.1% from 2.2% previously, after the U.S. Census Bureau reported that U.S. wholesale inventories fell 0.2% in August, compared to a decline of 0.1% previously reported. The Atlanta Fed has also reduced its forecast of third-quarter real government spending growth, from 0.1% to –0.1%, following the release of the disappointing nonfarm payrolls report.

Separately, the Federal Reserve Bank of New York revised its fourth-quarter 2016 GDP forecast 10 basis points upward on Friday, to 1.3% from 1.2% previously, while it kept the third-quarter 2016 GDP forecast at 2.2%, citing positive readings of international trade data, as well as the manufacturing and non-manufacturing ISM business surveys. Taking the latest New York Fed forecast into account, the pace of U.S. GDP annual growth could be about 1.4% year-on-year, the slowest compounded annual growth rate (CAGR) since the end of the deep recession in 2009. The current blue chip consensus U.S. GDP 2016 forecast is 1.8%.

For the week, the U.S. dollar index surged 1.33%, to close at 96.654 on Friday. The yield of 10-year U.S. Treasury Notes skyrocketed 8.12% for the week to close at 1.73%, while the yield spread between the 10-year and 2-year U.S. Treasury Notes climbed to 0.90 percentage points. The global bond markets continued their wide rides, as the 10-year JGB yield jumped 20.51% to negative 0.062% at the close on Friday, while the 10-year German bund yield turned positive, to close at 0.021%.

The WTI crude price surged another 3.25% for the week to close at $49.81 per barrel on Friday, while the Brent crude spot price jumped 3.3% to close at $51.68 per barrel, after a Reuters report said that Saudi, Iranian and Iraqi energy ministers will meet Russian energy minister Alexander Novak on the sidelines at the World Energy Conference in Istanbul next week.

The EIA weekly U.S. oil inventory report on Wednesday showed another decrease of 3 million barrels to 499.7 million barrels, excluding the Strategic Petroleum Reserve, in the week ending September 30, compared to S&P Global Platts analysts’ expectations for a rise of 2 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory decrease of 7.6 million barrels.

Separately, the EIA said the weekly U.S. crude oil production decreased by 30,000 barrels per day (bpd) for the week ending September 30, to 8.467 million bpd. Weekly U.S. crude oil output has fallen about 11.89% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose by 3 to 428, compared to 316, when the rig count hit the low on June 6, 2016.

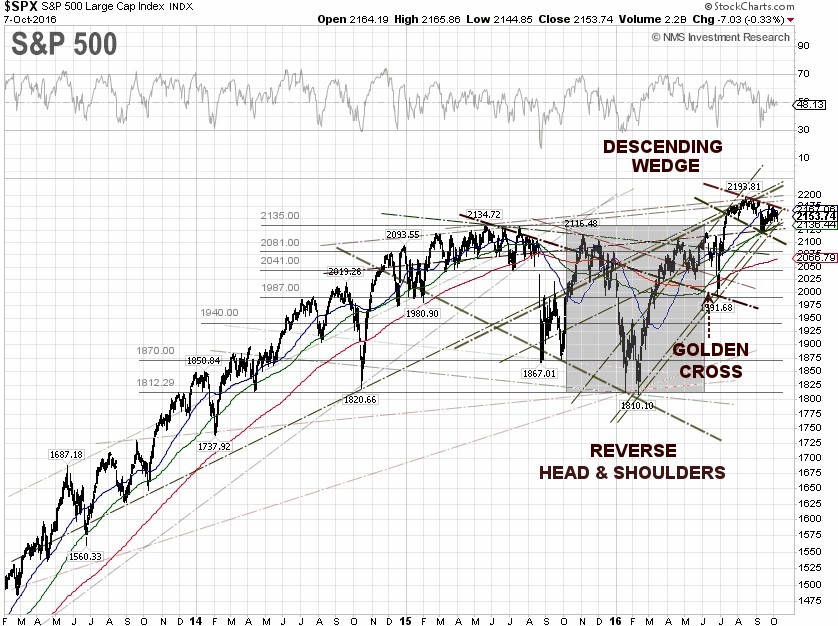

The best performing S&P 500 sectors for the week were Financials and Energy, up 1.52% and down 0.01%, respectively. The worst performing sectors for the week were Real Estate, Telecommunication services, and Utilities down 5.25%, 3.84% and 3.81%, respectively.

S&P 500 Summary: +5.37% YTD as of 10/07/16

Barclay Hedge Fund Index: +4.22% YTD

Outperforming Sectors: Energy +16.02% YTD, Information technology +10.99% YTD, Telecommunication services +9.42% YTD, Utilities +8.78% YTD, Materials +7.52% YTD, and Industrials +7.36% YTD.

Underperforming Sectors: Consumer staples +3.59% YTD, Consumer discretionary +2.03% YTD, Financials +1.22% YTD, Healthcare –0.20% YTD, and Real Estate –6.99%

YTD. |