|

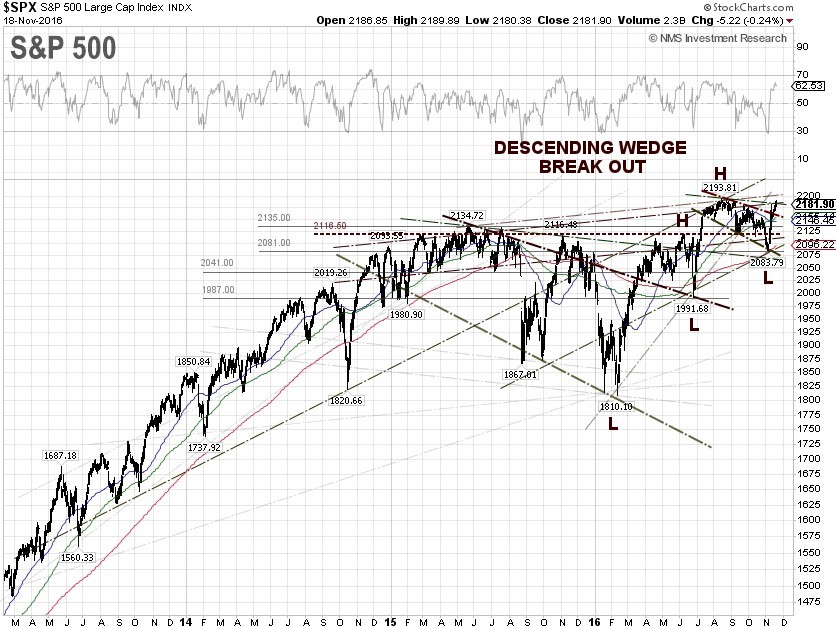

The S&P 500 gained 0.81% for the week, to close on Friday at 2,181.90, led to the upside by Telecommunication services and Financials. The Telecom sector continues to outperform as the market anticipates a new Republican FCC will make a big push to roll back some of the regulations put in place under President Obama, while a steeper yield curve drove the Financials sector. The U.S. Dollar index (DXY), practically the USD/EUR exchange rate, and Treasury yields rose sharply this week after Fed Chair Janet Yellen told U.S. Congress on Thursday that a Fed rate hike could come “relatively soon”.

St. Louis Federal Reserve President Bullard, a voting member of FOMC, told the audience at a conference in Frankfurt on Friday that, "Markets are currently putting a high probability on a December move by the FOMC. I'm leaning towards supporting that.", according to Reuters. Indeed, Wall Street wants to see the Federal Reserve raise the federal funds rate target to 50 and 75 basis points at the December 13-14 FOMC meeting, since the probability of a 25 basis point rate hike has already surged to 95.4%, based on the CME Group 30-day Fed Fund futures prices as of November 18. Failure to do so is no longer an option for the Fed.

For the week, the DXY rose another 2.25% to close on Friday at 101.28, a thirteen-year high. The strong U.S. dollar and the rise in Treasury yields, which are intended consequences of a Fed rate hike, will hammer U.S. exports and corporate earnings. According to data from the Bureau of Economic Analysis (BEA), U.S. exports of goods and services plunged from $597.8 billion in the third-quarter 2014 to a one-and-a-half year low of $538.9 billion in the first-quarter 2016, while the U.S. dollar appreciated about 10% against other major currencies during the same period.

Recent data released by the U.S. Department of the Treasury showed that China sold $83 billion worth of U.S. Treasury Securities between June and August and now holds about $1.157 trillion of U.S. Treasury Securities, as of September 2016. The yield of 10-year U.S. Treasury Notes continued to surge another 8.84% this week to close at 2.34% on Friday, while the yield spread between the 10-year and 2-year U.S. Treasury Notes widened to 1.27 percentage points. The resistance levels for the 10-year U.S. Treasury yield are 2.36% and 2.50%, respectively. The 10-year JGB yield turned positive for the week to 0.04% at the close on Friday, while the 10-year German bund yield dropped 12%, to close at 0.272%.

Separately, the Federal Reserve Bank of New York raised its fourth-quarter 2016 GDP forecast 80 basis points on Friday, to 2.4% from the previous 1.6% two weeks ago, citing positive data from retail sales and housing starts. Taking the latest New York Fed forecast into account, the pace of U.S. GDP 2016 annual growth will be just 1.56% year-on-year, the slowest growth since 2009. The number is well below the Federal Reserve's expectations of between 1.7 and 1.9%, according to the minutes from the September 20-21 FOMC meeting.

The WTI crude price jumped 6.80% this week, to close at $46.36 per barrel on Friday, while the Brent crude spot price surged 5.32% to close at $46.88 per barrel, despite a bearish EIA weekly U.S. oil inventory report. The WTI crude price surged 1.31% to an intraday high of $46.41 per barrel on Wednesday, after Russia's Energy Minister Alexander Novak said that he sees big chances for the Organization of the Petroleum Exporting Countries (OPEC) to reach an agreement to curb production, according to Reuters. Some OPEC members are now saying OPEC will do whatever it takes to make all members join the production cut agreement — willingly or unwillingly.

Part of the crude oil volatility this week was also due to the rollover of crude oil futures contracts on Thursday. The crude oil WTI Jan 17 contract (CLF7) became the lead contract as the Dec 16 contract (CLZ6) expires on Monday, November 21.

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies increased by 5.3 million barrels to 490.3 million barrels, excluding the Strategic Petroleum Reserve, in the week ending November 11, compared to S&P Global Platts analysts’ expectations for a decline of 2.0 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory increase of 3.65 million barrels.

Separately, the EIA said the weekly U.S. crude oil production dropped 11,000 barrels per day (bpd) for the week ending November 11, to 8.681 million bpd. Weekly U.S. crude oil output has fallen about 9.67% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose by 19 to 471, compared to 316, when the rig count hit the low on June 6, 2016.

The best performing S&P 500 sectors for the week were Telecommunication services and Financials up 3.02% and 2.24%, respectively. The worst performing sectors for the week were Healthcare and Consumer staples down 1.23% and 0.14%, respectively.

S&P 500 Summary: +6.75% YTD as of 11/18/16

Barclay Hedge Fund Index: +4.06% YTD

Outperforming Sectors: Energy +16.18% YTD, Financials +14.20% YTD, Industrials +13.95% YTD, Materials +10.51% YTD, and Information technology +10.37% YTD.

Underperforming Sectors: Utilities +6.27% YTD, Telecommunication services +5.90% YTD, Consumer discretionary +3.71% YTD, Consumer staples –0.26% YTD, Healthcare –3.52% YTD, and Real Estate –11.27%

YTD. |