|

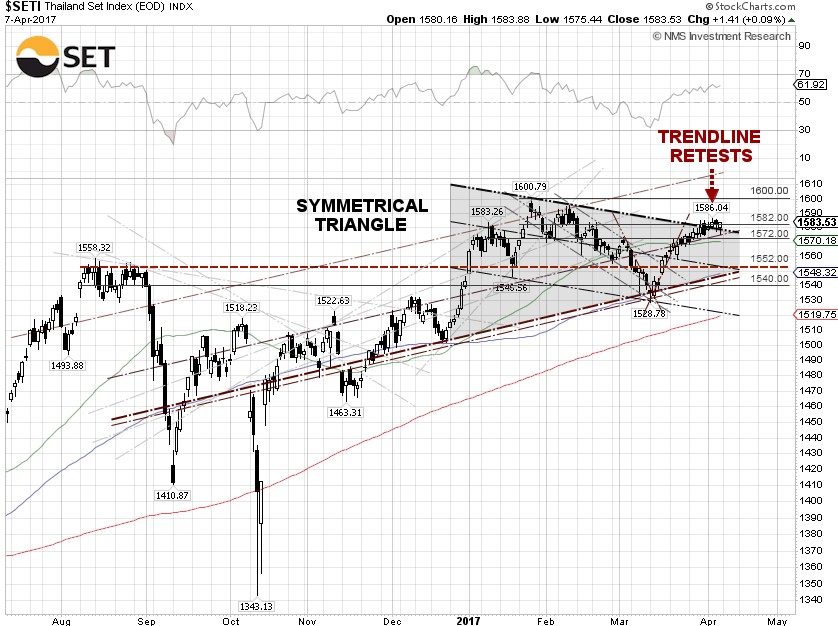

The SET index inched up 0.53% for the week, to close on Friday at 1,583.53, led by big cap stocks, including CP All PCL (SET:CPALL), Kasikornbank PCL (SET:KBANK), Siam Cement PCL (SET:SCC) and PTT PCL (SET:PTT), up 4.24%, 2.38%, 1.85%, and 1.29%, respectively. The SET index broke out the symmetrical triangle chart pattern on Tuesday and is retesting the trendline support, where the index could bounce off if a catalyst emerges. According to the SET market data, retail investors were net sellers during the first-week of April while Thai institutional and foreign investors were net buyers.

The USD/THB inched up 0.77% for the week to close on Friday at 34.615. The Bank of Thailand, or BOT, said on April 1 that the bank will start tapering its short-dated bond issuances this month by 80 billion baht to curb baht speculation, according to the Bangkok Post. A weak baht might have nothing to do with the BOT's intervention announcement, as the U.S. Dollar index (DXY), essentially the USD/EUR exchange rate, closed at 101.12 on Friday, up another 0.90% for the week, despite weak U.S. economic data and the March nonfarm payrolls report that missed expectations.

Currency speculators ran up the U.S. dollar and sold the British pound after Bank of England, or BOE, Governor Mark Carney hinted at the possibility of a ōhard Brexitö scenario at his speech at Thomson Reuters in London on Friday. To make matters worse on Friday, UK industrial production and manufacturing output came in short of expectations for February, contracting 0.7% and 0.1% for the month, respectively.

William C. Dudley, President of the Federal Reserve Bank of New York added fuel to the dollar fire after he said during Q&A at a luncheon in New York City on Friday that the Federal Reserve might in the future avoid raising interest rates at the same time that it begins the process of shrinking its $4.5 trillion bond portfolio, prompting only a "little pause" in the central bank's rate hike plans.

The yield of Thailand 10-year government bonds tumbled 2.02% for the week, to close at 2.665% on Friday. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 2.382% on Friday, narrowed to 0.283 percentage points. The spot gold price gained 0.49% for the week, to close at U.S. $1,257.30 per ounce on Friday, while the Japanese yen appreciated 0.26% against the U.S. dollar at 111.09 yen.

The WTI crude spot price surged 3.24%, closing at $52.24 per barrel on Friday, while the Brent crude spot price was up 2.93% to close at $55.19 per barrel, despite another bearish EIA weekly report. It sounds like Goldman Sachs is backstopping WTI crude prices, when the firm sent out a research note on Wednesday saying that with global demand exceeding supply, they are "constructive" on oil prices, at least in the short term. Goldman said, "We project WTI will increase from $50/bbl to $57.50/bbl by mid-year and average of $55/bbl in ōthe second half of 2017", according to Barrons.

Just about two weeks ago, on March 21, Goldman Sachs sent out a research note saying that 2017-19 is likely to see the largest increase in history for mega projects' production, as the record 2011-13 capex commitment yields fruit, meaning a possible record for non-OPEC production growth in 2018. The WTI crude spot price tumbled 1.37% that day to $48.24 per barrel, below the 200-day SMA. Crude oil prices were also given a boost after the U.S. launched cruise missiles at a Syrian base on Thursday, in response to a chemical weapons attack in Syria that killed more than 100 civilians earlier in the week.

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies increased by 1.57 million barrels to an all-time high of 535.54 million barrels, excluding the Strategic Petroleum Reserve, in the week ending March 31, compared to the Wall Street Journal forecast for a stockpile decline of 0.2 million barrels. The American Petroleum Institute, or API, inventory data on Tuesday showed a U.S. crude inventory decline of 1.8 million barrels.

Separately, the EIA said the weekly U.S. crude oil production increased 52,000 barrels per day, or bpd, for the week ending March 31, to 9.199 million bpd. U.S. crude oil output increased 137,000 bpd to an average of 9.134 million bpd in March, compared to a February average of 8.997 million bpd. Output has fallen just 4.85% from the peak level of 9.60 million bpd in June 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose another 10 to 672, compared to 316, when the rig count hit the low on June 6, 2016.

|