|

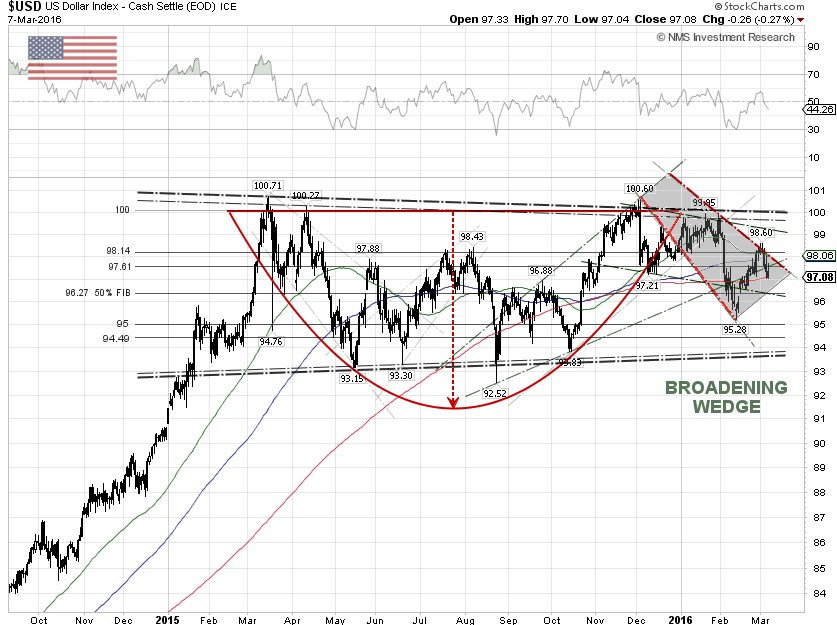

The U.S. dollar index (DXY), a weighted index of the value of the U.S. dollar relative to a basket of six major currencies, is on the rebound since it plunged to the February low of 95.28, after Federal Reserve Chair Janet Yellen told the U.S. Congress during her two-day semiannual monetary policy report, on February 10-11, that overseas weakness and market distress could threaten the Fed's plans to raise the rate, but didn’t explicitly mention any delays to interest rate hikes.

There are warning signs that something is wrong with the U.S. service sector, accounting for nearly 80% of the private sector gross domestic product (GDP), according to the Department of Commerce. A preliminary reading of the Markit Economics monthly flash services purchasing manager's index (PMI) for February released last month, came in at 49.8, missing the estimate of 53.5 by a wide margin. A reading below 50 means the service sector of the U.S. economy is in contraction.

The Institute for Supply Management (ISM) said earlier this month that its index of non-manufacturing activity fell to 53.4 in February, from 53.5 the previous month. The figure was barely above expectations of 53.2 from a Reuters poll of 81 economists. The ISM index has been on its downtrend since October 2015, when the reading was 59.1.

Despite that the U.S. labor market continues to strengthen, wages remain stagnant. The Labor Department said last week that there were 242,000 nonfarm payrolls jobs added in February, exceeding Wall Street economists’ forecast for a 190,000 job gain. The vast majority of jobs, about 150,000 however, came from healthcare, social assistance, retail, and food services, meaning low wages. This could explain why average hourly wages declined 3 cents to $25.35, following an increase of 12 cents in January.

As of March 1, there were 14,786 short positions of U.S. Dollar Index futures [DX], traded on the U.S. Intercontinental Exchange (ICE) in units of $1,000 x index value, by non-commercial or speculative, a decrease of 896 contracts from the previous week, according to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC). This is compared to about 41,571 long positions, a decline of 3,536 contracts during the same period. Hedge funds turned less bullish on the dollar ahead of the nonfarm payrolls report and reduced their net long positions by 2,640 contracts.

Dollar strength in late February has been fueled by speculations that the European Central Bank (ECB) is expected to cut its deposit rate by 10 basis points to – 0.4% at the Governing Council meeting in Frankfurt on March 10, but markets are split over what other steps are likely, said Reuters. Some predict an increase to the 60 billion euros per month asset buys, others see just technical changes to quantitative easing and some expect the bank to unveil a multi-tier deposit rate system.

The ECB’s move may not already be priced in, despite that President Mario Draghi has been making similar remarks over-and-over since the January Governing Council meeting in Frankfurt, saying the central bank won’t hesitate to boost its stimulus if it believes recent financial-market turmoil or lower oil prices could further weigh on eurozone inflation. According to CFTC data, hedge funds increased their euro FX short positions, traded on the Chicago Mercantile Exchange (CME), by about 16,096 contracts during the week ending March 1 where euro FX contracts are traded in units of 125,000 euros.

From our technical viewpoint, the U.S. dollar index has been consolidating since early January and thus the cup with handle chart pattern is still unconfirmed. In order to confirm the cup with handle chart pattern, the index needs to break out the top trendline resistance of the descending broadening wedge chart pattern soon, or the DXY could pull back to the 94 and 95 levels.

The DXY could start losing momentum fast, after the ECB meeting, as the strength of the dollar has been fueled by expectations of aggressive easing by the ECB. One of the U.S. Federal Reserve's most prominent advocates of higher interest rates, James Bullard, the president of the Federal Reserve Bank of St. Louis, recently declared that it was "unwise" to move any further in light of weak inflation and global volatility, suggesting the Fed is stepping further away from plans to continue to hike rates, said Reuters.

Nearly 68% of economists surveyed by Bloomberg now say that the Fed’s next rate hike will be at the FOMC meeting in June. In January, only 30% of those surveyed had thought that the Fed would increase in June, with the majority believing in a March rate hike. |